Embedded finance Southeast Asia: How software companies launch a second revenue line

Embedded finance is not a future adjacency for software companies; it is a second revenue line unlocked the moment you have weekly engagement, money flowing through your product, and user trust to hold a balance.

Embedded finance has been marketed to VCs and bank executives for the last five years. But almost no one has really explained it well to the people who can actually launch it. The reason you don't know this is possible isn't that it's new. It's that the people selling it have been selling to the wrong audience.

A software company in Southeast Asia can launch financial products on top of its existing product. Wallets. Cards. Lending. The constraint is not licensing or infrastructure. The constraint is whether your product already creates the conditions for money to live inside it.

Three conditions determine that:

(1) You have users who come back weekly;

(2) You have money that already flows through your product; and

(3) A brand they would trust to hold their balance.

If those three are true, continue to read along.

The first movers already crossed over.

The largest consumer platforms in Southeast Asia no longer treat fintech as an experiment.

Sea’s digital financial services arm generated $2.4 billion in 2024 revenue, up 35% year-on-year, with a $5.1 billion loan book and 1.2% 90-day delinquency. That line is now larger than its original business.

Grab’s financial services revenue reached $253 million, up 44%, with $1.43 billion in deposits. It is the fastest-growing segment in the company.

GoTo’s fintech business generated roughly $225 million, up 95%, and turned profitable in Q4.

None of these companies started as banks. Each one built a high-frequency surface first, then layered financial products on top of existing behavior. Distribution came first. Financial services followed.

That same architecture is now available to companies at a fraction of their scale.

Most operators in Southeast Asia still think it is not.

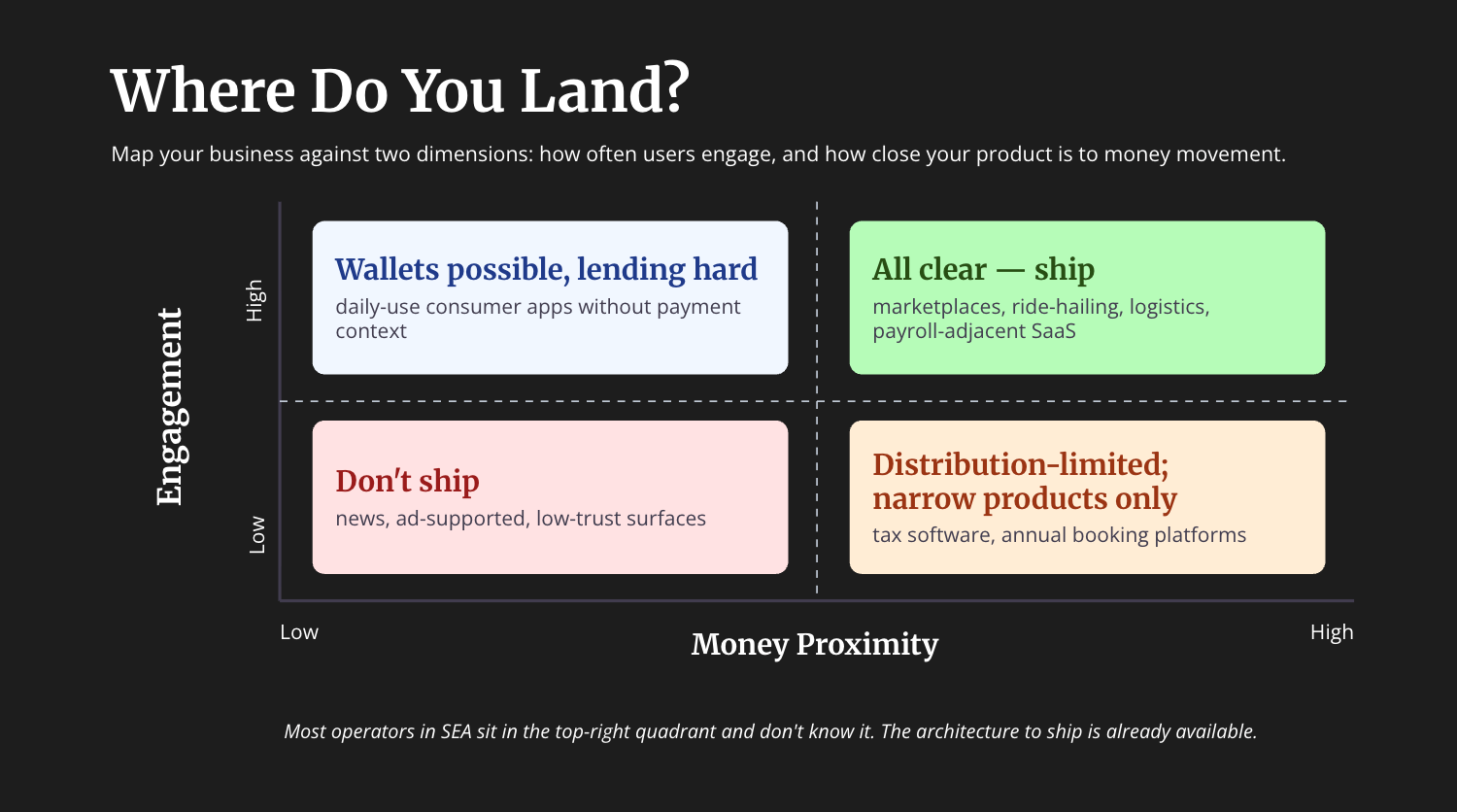

The three tests

Most companies fail qualification. The question is not ambition. The question is structural fit.

Engagement defines whether a wallet has somewhere to live. Weekly usage is the floor. Daily usage compounds. Infrequent products cannot support stored value.

Money proximity determines whether you have leverage. Payments, bookings, payroll, invoicing, payouts. These moments generate transaction data and insertion points. Without them, you are guessing.

Trust sets the ceiling. If holding a balance feels unnatural in your product, distribution fails immediately. Trust is upstream. It comes from being the system of record for something users already rely on.

All three must be true.

Two out of three produces a narrow product with limited expansion. One out of three produces a feature, not a business.

Napkin math

Run a base case.

10,000 MAU. Four transactions per user per month. ₱2,500 average ticket size. ₱100 million in monthly GMV.

Capture 30% of that flow through a wallet in year one. That produces ₱30 million in captured volume.

Apply a 1% take rate. ₱300,000 in monthly revenue.

Apply a 1.5% annual float yield. ₱37,500 per month.

Total: ₱337,500 monthly from a product built on top of existing behavior.

If software ARPU is ₱500, core revenue is ₱5 million per month. The financial layer contributes 6.75%.

Scale to 50,000 MAU with the same assumptions. The financial layer contributes 33.75%.

This is not incremental revenue. This is the line that changes your margin profile.

You do not need Grab-scale GMV. You need captured flow.

What changed

This used to require a bank partnership. Timelines ran 18 to 24 months. Economics skewed heavily to the bank. Execution required balance sheet, regulatory patience, and executive alignment.

That path still exists but it is no longer the default.

Banking-as-a-Service providers absorb licensing, compliance, and core infrastructure. Teams integrate via API. Time to launch compresses to roughly three months. Customer acquisition cost drops from $100–200 to about $35 for embedded users.

Time, CAC, and capex collapsed simultaneously. The cost to ship financial products dropped by an order of magnitude in three years.

The people who said "we'll do fintech later" three years ago were right. "Later" is now. The build that used to cost a year and a balance sheet now costs a quarter and an integration.

What to decide this week

Do users return weekly. Does money flow through the product. Would users trust you to hold a balance.

If all three are true, the decision is sequencing.

Start with the product that sits closest to existing behavior. Wallet if you already intermediate payments. Payment links if you orchestrate transactions. Cards if you control spend. Capital if you see cash flow.

The question is not whether to become a fintech.

The question is how much of your second revenue line you will ship this year.

Most teams will just ignore it 🤷♂️