Most Southeast Asian Businesses Aren’t Built for Venture Capital

The founders who win aren’t the ones who raise the biggest checks—they’re the ones who know exactly what game they’re playing and have the courage to run it on their own terms.

Southeast Asia lacks serious calibration. In the first half of 2025, the region raised $1.85 billion across 229 deals, the weakest showing in over six years.

Yet the narrative remains stubbornly the same: "We need more funding." More accelerators. More pitch competitions. More demo days modeled after Y Combinator.

I've sat through so much of these pitches and it's striking that most founders are building businesses that make perfect sense.....as a lifestyle business, not growth companies.

It's not that we lack ambition or technical chops. It's that we've imported Silicon Valley's playbook without questioning whether our businesses qualify for it.

When I started out, I thought every startup should raise venture capital. But I've seen founders "think big", dream unicorn valuations, and optimize for hyper growth. Then you get to see the same founders flame out within four years because the pressure of venture scale becomes an impossible task.

We're solving the wrong problem. The issue isn't capital access—it's knowing whether you should take it at all.

The Western Playbook

For over a decade, Southeast Asia has been marinating in Silicon Valley orthodoxy. Raise a seed round. Build an MVP. Get to product-market fit. Raise Series A. Scale fast and break things. The gospel spread through Medium posts, Y Combinator videos, and well-meaning advisors who'd never actually operated in the region.

The result? A generation of founders optimizing for metrics that don't match their business models.

They weren't building platforms; they were digitizing services.

They didn't have network effects; they had operational leverage that scaled linearly with headcount.

They weren't creating software; they were assembling teams to execute repetitive tasks with better branding.

Most global venture capital data shows that only a small minority of VC-backed startups generate significant investor returns, with many either closing or merely returning the original investment, underscoring that fundraising isn't proof your business is built for exponential growth.

VC operates on power law dynamics: expect nine failures, hope for one 100x return that carries the entire fund.

Still, some founders think venture capital is validation, when in reality, funding is not proof of fitness—it's a bet on exponential outcomes that most businesses cannot and should not pursue.

The Venture-Suitability Framework

The region badly needs a mirror. A self-diagnostic that forces founders to ask: "Is my business actually built for venture capital, or am I chasing funding because that's what startups are 'supposed' to do?"

The Venture-Suitability Framework: a simple eight-criteria diagnostic tool that separates genuinely scalable ventures from well-intentioned businesses that should bootstrap, profitably grow, or seek alternative financing.

And in a market where funding has mostly evaporated, founders need to know whether they're building a rocket ship or a really nice bicycle.

The framework clusters into four fit categories: Market Fit, Product Fit, Channel Fit, and Model Fit.

Market Fit

- Large Addressable Market (TAM): Is your total addressable market $1B+ with a realistic path to capturing 5-10%?

- Market Timing & Dynamics: Are you riding a secular shift or solving an emerging pain point with favorable tailwinds?

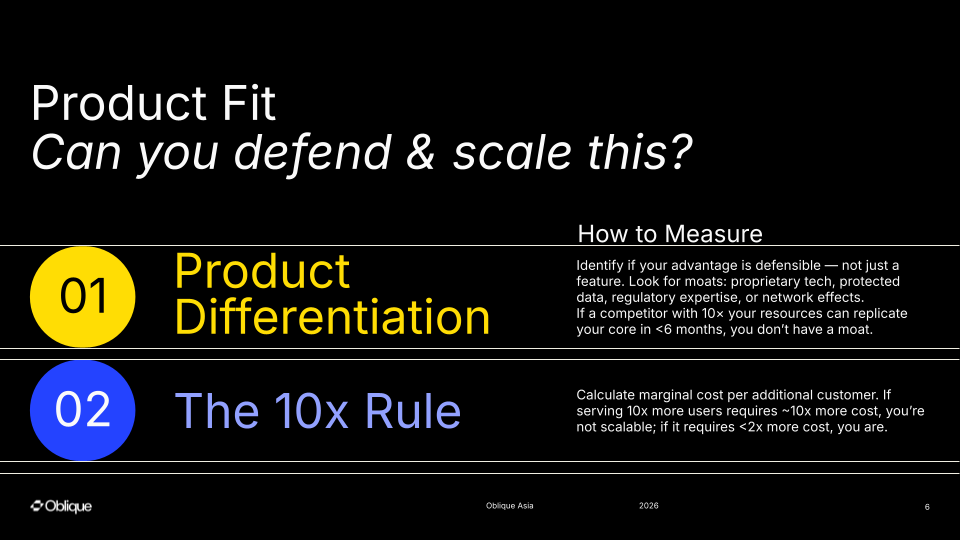

Product Fit

- Product Differentiation: Do you have defensible IP, proprietary technology, or a solution that's 10x better than alternatives?

- Technical Scalability: Can you grow 10x without proportionally increasing headcount or infrastructure costs?

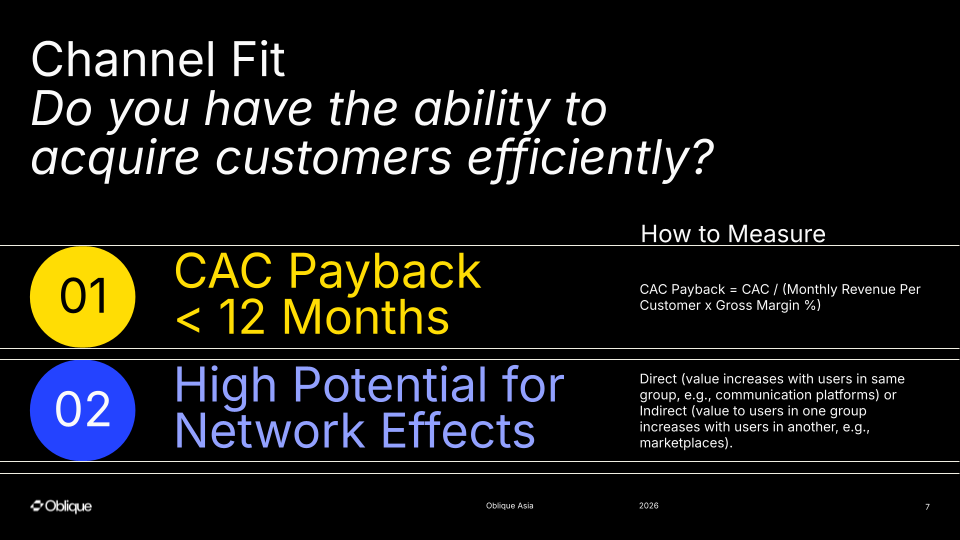

Channel Fit

- Favorable Unit Economics: Is your LTV:CAC ratio above 3:1, with CAC payback under 12 months and gross margins exceeding 70%?

- Network Effects Potential: Does each new user increase the value for existing users, creating organic viral growth?

Model Fit

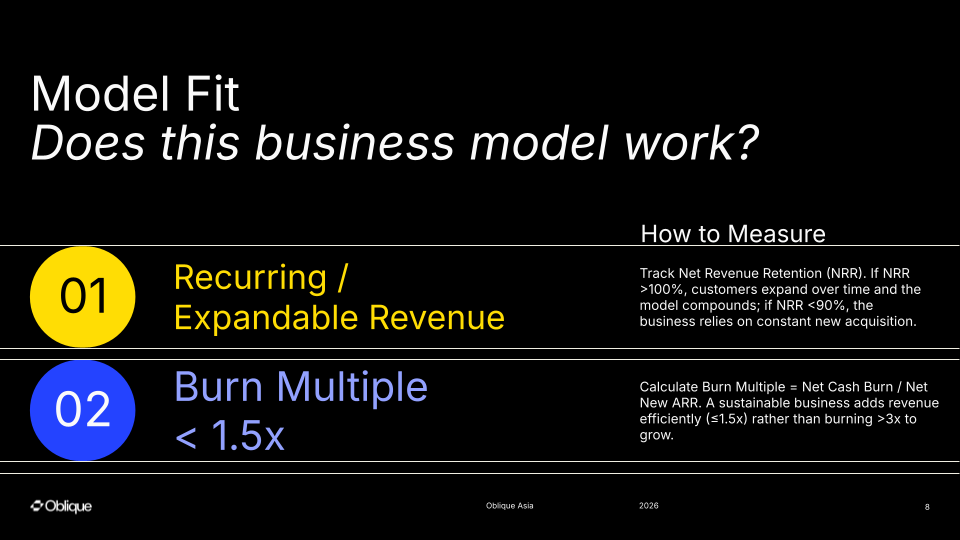

- Recurring Revenue Model: Can you generate predictable, subscription-based revenue streams?

- Capital Efficiency: Can you articulate a clear path to your next value inflection point (profitability, $1M ARR, or Series A readiness) with reasonable capital requirements relative to your market?

Pass fewer than six? You might be building a great business—just not one suited for venture capital. Here's a deep dive:

Market Fit: Is the Ocean Big Enough?

Large Addressable Market

The first filter every serious investor applies. Venture funds need portfolio companies capable of reaching $100M+ in revenue to generate meaningful returns. If your total addressable market (TAM) is under $1 billion, or your serviceable addressable market (SAM) is under $100 million, the math simply doesn't work for institutional capital.

Where most founders stumble: they confuse "market need" with "market size."

Yes, small restaurants in Manila need better inventory software. But if there are only 15,000 such restaurants and they'll each pay $50/month maximum, your SAM caps at $9 million annually. That's a perfectly viable lifestyle business, but it's not venture-scale.

The trap: Founders overestimate TAM by using top-down math ("The restaurant software market is $50B globally!") without doing bottom-up segmentation. Real TAM analysis starts with your specific customer profile, then multiplies upward based on realistic penetration.

Market Timing & Dynamics

Are you riding a secular shift, like on-premise to cloud, or fighting entrenched behaviors? The best outcomes occur when at least three macro tailwinds align: regulatory change, tech inflection, and shifting consumer behavior.

The best venture outcomes occur when three or more macro tailwinds align: regulatory change, technology inflection points, and shifting consumer behavior. Grab succeeded not just because it built a better taxi app, but because smartphone penetration, mobile payments infrastructure, and urbanization all converged simultaneously.

The trap: Mistaking a temporary COVID bump for a secular trend. Countless food delivery and remote work startups raised in 2020-2021 based on pandemic usage that collapsed when offices reopened.

Product Fit: What Makes You Defensible?

Product Differentiation

This determines whether you're building a moat or a sandcastle. Investors want to see proprietary technology, patents, unique datasets, or network effects—something that prevents competitors from replicating your solution in six months.

In Southeast Asia's B2B SaaS landscape, the most defensible companies are those solving vertical-specific problems that require deep industry knowledge. Mekari in Indonesia didn't just build accounting software; they embedded compliance logic specific to Indonesian tax regulations, making them sticky with SMEs who can't easily switch.

The trap: Confusing features with defensibility. "We use AI/blockchain" is adoption, not a moat. What would it take for a competitor with 10x your resources to copy you? If six months and $500K would do it, you don't have a moat.

Technical Scalability

This is the multiplier that separates venture businesses from service businesses. Can you grow revenue 10x without scaling costs 10x? Software achieves this—one codebase serves thousands. Manual-heavy services can't. An example is a logistics startup that manually coordinates deliveries needs proportionally more dispatchers, drivers, and customer support reps as order volume grows.

The trap: Most "tech-enabled" startups in Southeast Asia are actually service businesses with a mobile app wrapper. They have linear cost structures disguised as platforms. A courier aggregation app that relies on human dispatchers hasn't solved the scalability problem—it's just digitized an operations team.

Channel Fit: The Economics of Growth

Favorable Unit Economics

This might be the most brutally honest criterion on this list. It asks: do you make money on each customer, and can you acquire customers profitably?

The Gold Standard:

- LTV/CAC > 3:1

- CAC payback < 12 months

- Gross margins > 70% (SaaS often hits this, logistics/e-commerce typically cap at 20-30%).

SaaS companies with annual contracts can often hit these benchmarks. E-commerce and logistics companies rarely can, because their gross margins cap at 20-30% and customer acquisition costs remain stubbornly high.

Here's what founders need to internalize: negative unit economics don't magically fix themselves at scale. If you lose $5 on every order, you can't make it up in volume. You just lose money faster.

The trap: Subsidizing growth with investor capital and calling it "capturing market share." This works only if you're in a winner-take-all market with clear network effects (like ride-hailing). For most businesses, it's just burning cash to buy revenue that disappears the moment you stop subsidizing it.

Network Effects Potential

This is the holy grail of venture scalability. True network effects mean each new user increases product value for all users.

Marketplaces (Grab, Carousell), social platforms (Facebook), and communication tools (WhatsApp) have this. Most B2B SaaS does not.

Direct: Users directly benefit from others joining.

Indirect: More iPhone users bring in more developers, increasing overall product value.

The trap: Claiming "network effects" when you really just mean "customer referrals" or "brand awareness." Real network effects create exponential value curves and defensibility. Referral programs create linear growth.

Model Fit: The Business Fundamentals

Recurring Revenue Models

Predictable, subscription-based revenue is prized by investors. Transactional businesses must re-earn revenue every period and struggle to attract VC.

One-time transaction businesses—even profitable ones—struggle to attract venture capital because revenue must be re-earned every period. A SaaS company with $1M ARR (annual recurring revenue) and 95% retention knows it starts next year with $950K in the bank. An e-commerce company with $1M in annual sales starts next year at zero.

The trap: Adding a “subscription tier” to a transactional model and calling it SaaS. Investors know the difference.

Capital Efficiency

This the final reality check. Can you reach the next value inflection point—whether that's profitability, $1M ARR, or Series A readiness—without raising more money?

In the 2021 funding frenzy, capital efficiency barely mattered. Founders could raise on decks and promises. In 2025, Investors want to see a clear path to breakeven or proof that each dollar raised generates measurable progress toward market leadership.

The trap: Assuming you can always raise the next round. The funding environment is cyclical, and many startups that seemed "on track" in 2021 are now struggling to extend runways as Series A timelines stretch from 12 months to 36 months.

Venture Suitability Scorecard

Market Fit

| Criteria | Score (0–2) | Definition |

|---|---|---|

| TAM ≥ $1B | 0 = < $100M; 1 = $100M–$999M; 2 = ≥ $1B | Is the market large enough for venture-scale outcomes? |

| Market Timing & Competitive Dynamics | 0 = Poor timing / crowded; 1 = Neutral; 2 = Favorable / defensible | Are structural shifts creating an opportunity you can win? |

Product Fit

| Criteria | Score (0–2) | Definition |

|---|---|---|

| Product Differentiation | 0 = Parity; 1 = Better; 2 = Clear 10× advantage | Is the advantage defensible beyond features? |

| Technical Scalability | 0 = Linear scaling; 1 = Some economies of scale; 2 = Near-zero marginal cost | Can the product scale without proportional cost? |

Channel Fit

| Criteria | Score (0–2) | Definition |

|---|---|---|

| CAC Payback | 0 = >24 months; 1 = 12–24 months; 2 = <12 months | Is acquisition efficient enough for VC growth? |

| Network Effects Potential | 0 = None; 1 = Some; 2 = Strong | Does the product get more valuable as usage increases? |

Model Fit

| Criteria | Score (0–2) | Definition |

|---|---|---|

| Recurring / Expandable Revenue | 0 = One-time; 1 = Some recurring; 2 = High recurring / NRR ≥ 100% | Does revenue compound over time? |

| Capital Efficiency (Burn Multiple) | 0 = >3×; 1 = 1.5×–3×; 2 = ≤1.5× | Are you adding ARR efficiently relative to burn? |

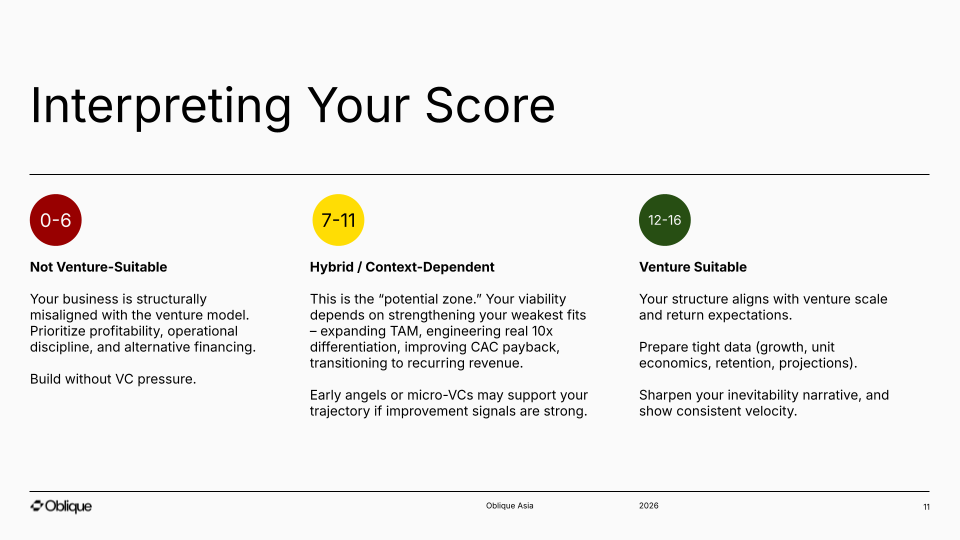

If you score 12 or higher: congratulations, you're building a genuinely venture-backable company. Optimize your pitch, refine your metrics, and find the right investors who understand your market.

If you score 7-11: you're in the gray zone. You might be able to raise from angels or regional micro-VCs, but institutional Series A will be challenging. Consider whether bootstrapping to stronger metrics, or pivoting your model toward greater scalability, makes sense.

If you score below 6: embrace it. You're building a business, not a venture. That's not failure—it's clarity. Bootstrap, optimize for profitability, take on strategic partners, or explore revenue-based financing. But stop trying to fit into a funding model designed for a different type of company.

Why This Matters Now

Southeast Asia's funding winter is a correction. Founders raised on growth narratives without unit economic discipline. Investors deployed capital into markets they didn't understand, using Silicon Valley heuristics that didn't translate.

The funding decline is forcing a reckoning. Investors are demanding profitability timelines, positive unit economics, and clear paths to exits. The founders who survive won't be those with the best pitch decks—they'll be those who built venture-suitable businesses.

This doesn't mean Southeast Asia lacks potential. The region still has 440 million internet users, rising middle-class consumption, and underserved markets across fintech, healthcare, education, and logistics.

What it means is that the playbook has to change.

Not every problem needs a venture-backed solution. Not every founder should optimize for unicorn outcomes. And certainly not every business with a mobile app qualifies as a "tech startup."

The most important realization? There's honor in building a profitable, sustainable business that serves customers well and employs people meaningfully.